IRS Deadlines That Can Change the Outcome of Your Case

This is a subtitle for your new post

Many IRS notices include deadlines that seem routine. Thirty days to respond. Sixty days to appeal. Ninety days to file a petition.

Because these notices often contain technical language and unfamiliar procedures, it is easy to assume that the deadlines are flexible or negotiable. In many cases, they are not.

Certain IRS deadlines determine whether important rights remain available. Missing one does not necessarily end the case, but it can change the options available to resolve it.

Understanding which deadlines matter most can make a significant difference in how an IRS case develops.

Some IRS Deadlines Determine Your Rights

Several deadlines within the IRS system control whether a taxpayer can challenge an action before enforcement begins. These deadlines are established by statute and are generally applied very strictly.

Here are three of the most important.

- 90 Days – Petition the U.S. Tax Court

When the IRS issues a Notice of Deficiency, the taxpayer generally has 90 days to file a petition with the United States Tax Court. Filing within this window allows the taxpayer to challenge the IRS's determination before paying the disputed tax.

This rule is established under

Internal Revenue Code §6213:

https://www.law.cornell.edu/uscode/text/26/6213

If the deadline is missed, the IRS may assess the tax and begin collection. At that point, the taxpayer typically must pay the tax first and then pursue a refund claim to challenge the liability. For that reason, the 90-day Tax Court deadline is one of the most rigid deadlines in the IRS system.

2. 30 Days – Request a Collection Due Process Hearing

When the IRS issues a Final Notice of Intent to Levy, the taxpayer generally has 30 days to request a Collection Due Process (CDP) hearing. A timely request allows the case to be reviewed by the IRS Independent Office of Appeals and typically suspends collection activity while the appeal is pending.

The rules governing this process are established under

Internal Revenue Code §6330:

https://www.law.cornell.edu/uscode/text/26/6330

If the deadline is missed, the IRS may proceed with collection actions such as levies. The taxpayer may still request an equivalent hearing, but some procedural protections are no longer available.

3. 60 Days – Appeal a Trust Fund Recovery Penalty Proposal

When the IRS proposes the Trust Fund Recovery Penalty for unpaid payroll taxes, it generally sends Letter 1153, giving the taxpayer 60 days to request an appeal. This may be the most important opportunity to challenge whether a person is considered responsible for the payroll tax liability. If no appeal is filed within that period, the IRS may assess the penalty and pursue collection against the individual.

Why Timing Matters in IRS Cases

Many IRS cases develop gradually. A notice arrives, a deadline passes, and the next notice appears with a firmer tone. Over time, these steps move the case closer to enforcement.

Recognizing the significance of these deadlines early allows taxpayers to respond deliberately rather than react after important rights have expired. In IRS matters, timing often matters just as much as the numbers themselves.

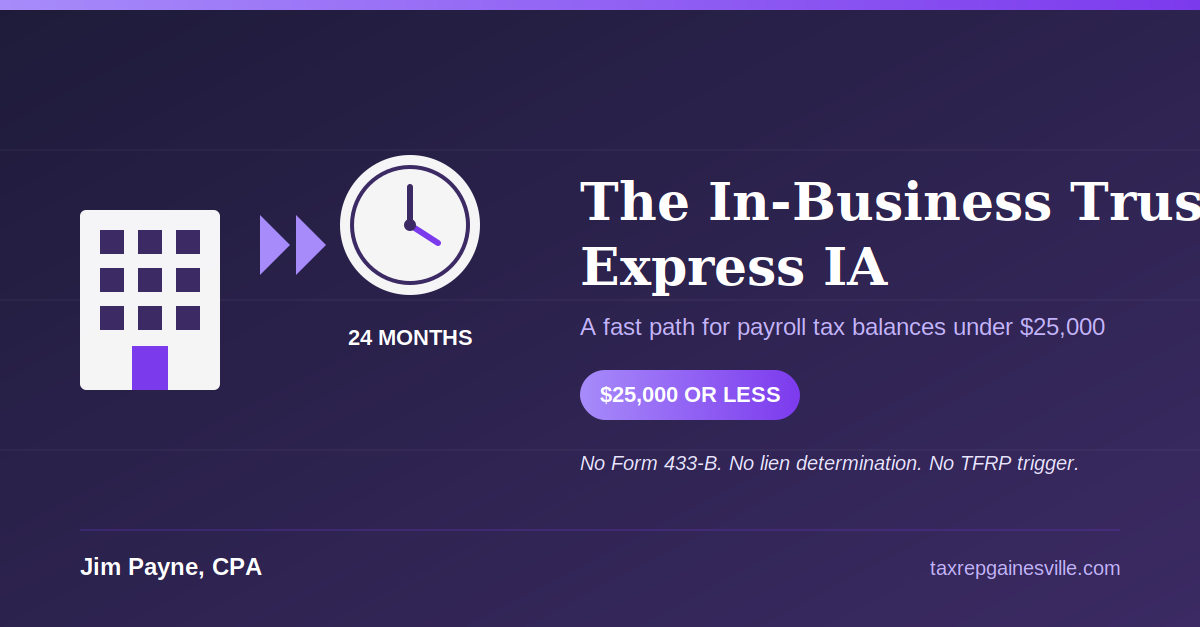

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances