Blog

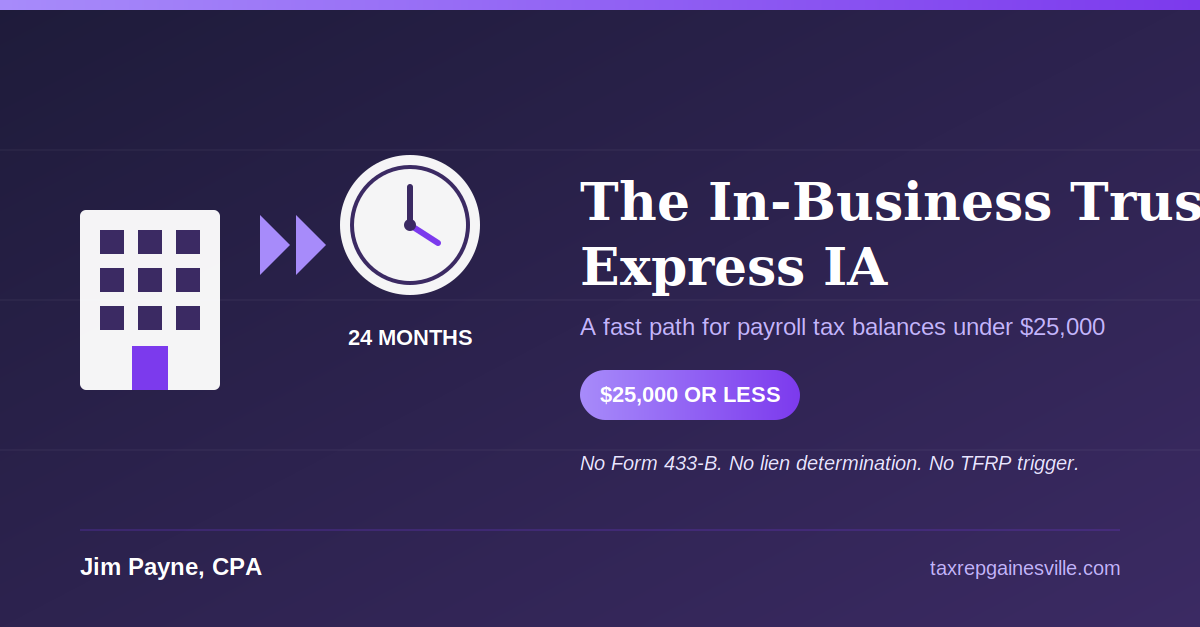

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances

Owe $25,000 or less in business payroll tax? Learn how the IRS In-Business Trust Fund Express Installment Agreement can resolve it in 24 months.

When a single-owner corporation files an OIC, the IRS runs two RCP analyses — and the owner gets squeezed twice. Here's how IRM 5.8.5 creates the trap and how to navigate it.

The IRS Pre-Qualifier Tool misleads clients. What actually determines OIC acceptance is the IRM 5.8.5 RCP calculation — and most self-prepared offers get it wrong.

A timely CDP request pauses levies, opens collection alternatives, and preserves Tax Court rights. Most practitioners don't use it to full effect — here's how.

The IRS TFRP investigation targets personal liability early. Know IRM 5.7.3's responsibility and willfulness standards before your client's Form 4180 interview.

business installment agreement lives or dies on the 433-B. Here's what trips up most referrals — and how to set your client up for approval.

A CP504 is not the final levy notice — but the IRS can already hit your client's state refund. Here's what to do in the next 30 days before the stakes get higher.

The IRS charged penalties and interest during COVID that the law says it shouldn't have. You may have until July 10, 2026, to get that money back.

Innocent spouse relief assumes joint liability already attached. But what if the joint return was never valid? Here's an overlooked angle for family law attorneys.

When your divorce client faces IRS liability from a joint return, IRC §6015 may offer relief — but a 2-year deadline applies. Here's what family law attorneys need to know.