How the IRS Decides Who Is Personally Responsible for Payroll Taxes

This is a subtitle for your new post

When payroll taxes go unpaid, the liability does not always stop with the business.

Many business owners are surprised to learn that the IRS can assess certain payroll taxes personally against individuals. This is called the Trust Fund Recovery Penalty (TFRP), and it applies to the portion of payroll taxes withheld from employees.

Understanding how the IRS decides who is responsible helps reduce confusion—and prevents costly mistakes during an investigation.

What the Trust Fund Recovery Penalty Covers

When an employer withholds federal income tax and FICA from employee wages, those funds are considered trust fund taxes. The employer is holding that money in trust for the government.

If those funds are not paid over to the IRS, Internal Revenue Code §6672 allows the IRS to assess the unpaid trust fund portion personally against certain individuals.

https://www.law.cornell.edu/uscode/text/26/6672

Importantly, this penalty does not include the employer’s matching portion of payroll taxes. It applies only to the withheld amounts.

The IRS Looks at Two Factors: Responsibility and Willfulness

To assess the Trust Fund Recovery Penalty, the IRS must determine that a person was:

- Responsible, and

- Willful in failing to pay the taxes.

Responsibility is not based on job title alone. The IRS looks at practical authority within the business, including:

- Who had the authority to sign checks

- Who controlled payroll decisions

- Who had authority over bank accounts

- Who decided which creditors were paid

Willfulness does not require bad intent. It generally means the person knew (or should have known) that payroll taxes were unpaid and allowed other bills to be paid instead.

These standards are explained in the Internal Revenue Manual under IRM 5.7.3 – Trust Fund Compliance: https://www.irs.gov/irm/part5/irm_05-007-003

The Form 4180 Interview

If a payroll case progresses, the IRS may conduct an interview using Form 4180, which documents the individual’s role in the business.

The purpose of the interview is to determine responsibility and knowledge. The answers given during this stage often shape whether the penalty is proposed.

Receiving a request for a Form 4180 interview does not mean the penalty has already been assessed—but it does mean the investigation is underway.

Not Everyone in the Business Is Automatically Liable

Multiple individuals can be assessed the Trust Fund Recovery Penalty. The IRS may assess it against more than one person if each meets the responsibility and willfulness tests. However, not every officer, manager, or employee qualifies as a responsible person. Authority and actual control matter.

Why Early Attention Matters

Once the Trust Fund Recovery Penalty is assessed, it becomes a personal liability. At that point, the IRS can pursue collection against personal bank accounts, wages, or assets.

Understanding how the IRS evaluates responsibility allows business owners and managers to approach the situation deliberately rather than reactively. Payroll tax cases escalate in stages. Knowing where the case stands—and who may be exposed—makes a significant difference in how it is handled.

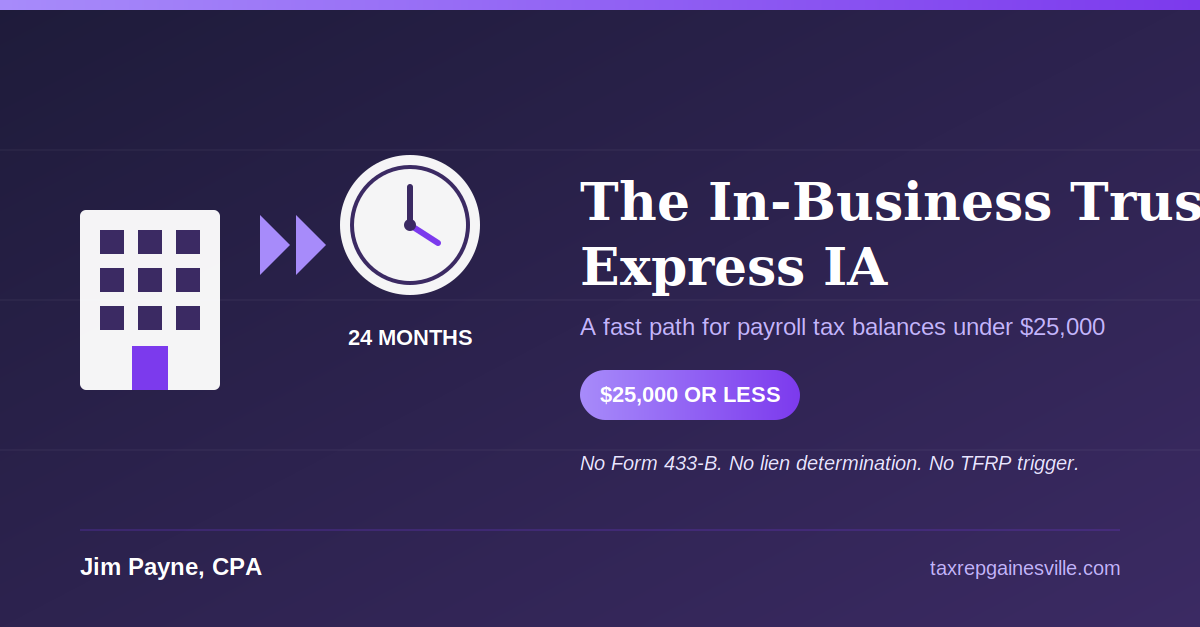

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances