Streamlined vs. Non-Streamlined IRS Installment Agreements

This is a subtitle for your new post

When a client owes back taxes and can't fully pay, an installment agreement is often the first resolution tool on the table. But "installment agreement" isn't a single product — the IRS operates multiple tracks depending on how much is owed, whether the taxpayer is an individual or business, and whether financial disclosure is required. Understanding which track applies and how to keep a client on the most favorable one is where representation adds real value.

The Governing Framework

The IRS's authority to enter into installment agreements flows from IRC § 6159, which permits the Service to accept payment of tax liabilities in installments when it determines that doing so will facilitate collection. The procedural rules governing how agreements are structured, approved, and monitored are found primarily in IRM 5.14.1 (Overview of Installment Agreements) and IRM 5.14.5 (Streamlined, Guaranteed, and In-Business Trust Fund Express Installment Agreements).

The key variable sorting clients into tracks is the total balance owed — combined tax, penalties, and interest across all open modules.

The Guaranteed Installment Agreement

For individuals owing $10,000 or less (excluding penalties and interest), the IRS is statutorily required to accept an installment agreement under IRC § 6159(c), provided the taxpayer meets specific conditions. Per IRM 5.14.5.2, those conditions are: all required returns have been filed; the taxpayer has not had an installment agreement in the prior five years; the taxpayer agrees to full payment within three years; and the taxpayer agrees to stay current on all future obligations.

No Collection Information Statement (CIS) is required. The IRS does not have discretion to reject a qualified request. For the right client, this is the cleanest possible path — no financial disclosure, mandatory acceptance, and a defined three-year window.

The Streamlined Installment Agreement

The more commonly used track for individuals is the Streamlined Installment Agreement, available for balances of $50,000 or less. Under IRM 5.14.5.1, the IRS will grant a streamlined agreement without requiring the taxpayer to submit a Collection Information Statement, provided the agreement calls for full payment within 72 months or before the Collection Statute Expiration Date (CSED), whichever is earlier.

For balances between $25,000 and $50,000, the IRS requires the agreement to be set up as a Direct Debit Installment Agreement (DDIA) — payments automatically withdrawn from a bank account. This is a condition of the streamlined track at that balance level; it is not optional.

Because no financial disclosure is required, the IRS is not analyzing the taxpayer's assets or income to determine a "correct" payment amount. The taxpayer and representative have considerably more control over the monthly payment figure, subject only to the requirement that the balance will be paid within the statutory window. This is a significant practical advantage.

One important planning note: if a client's aggregate balance is near the $50,000 threshold, it is worth evaluating whether any portion can be addressed before submitting the IA request — through a partial payment, application of a pending refund, or other means — to keep the case on the streamlined track and avoid financial disclosure entirely.

The Non-Streamlined Installment Agreement

When the balance exceeds $50,000, the case moves to the non-streamlined track. The rules shift considerably. Under IRM 5.14.1.4, the IRS is no longer obligated to accept the agreement and is not bound by the 72-month payment window. The revenue officer or ACS representative will evaluate the taxpayer's ability to pay based on a fully completed Collection Information Statement — Form 433-A for individuals, Form 433-B for businesses — along with supporting financial documentation.

The IRS will apply its standard allowable expense methodology (National Standards, Local Standards, and Other Necessary Expenses under IRM 5.15.1) to determine what it views as the taxpayer's monthly disposable income. It will then propose an agreement based on that figure, typically structured to pay off as much of the liability as possible before the CSED. The IRS also retains the right to request updated financial information periodically and to modify the payment terms if the taxpayer's financial condition improves (IRM 5.14.2.1).

Representation matters most at this stage. The CIS preparation, documentation of allowable expenses, and negotiation of a sustainable payment figure are precisely where a practitioner protects the client's long-term interests. A payment set too high — even if technically within the client's means in a good month — creates default risk.

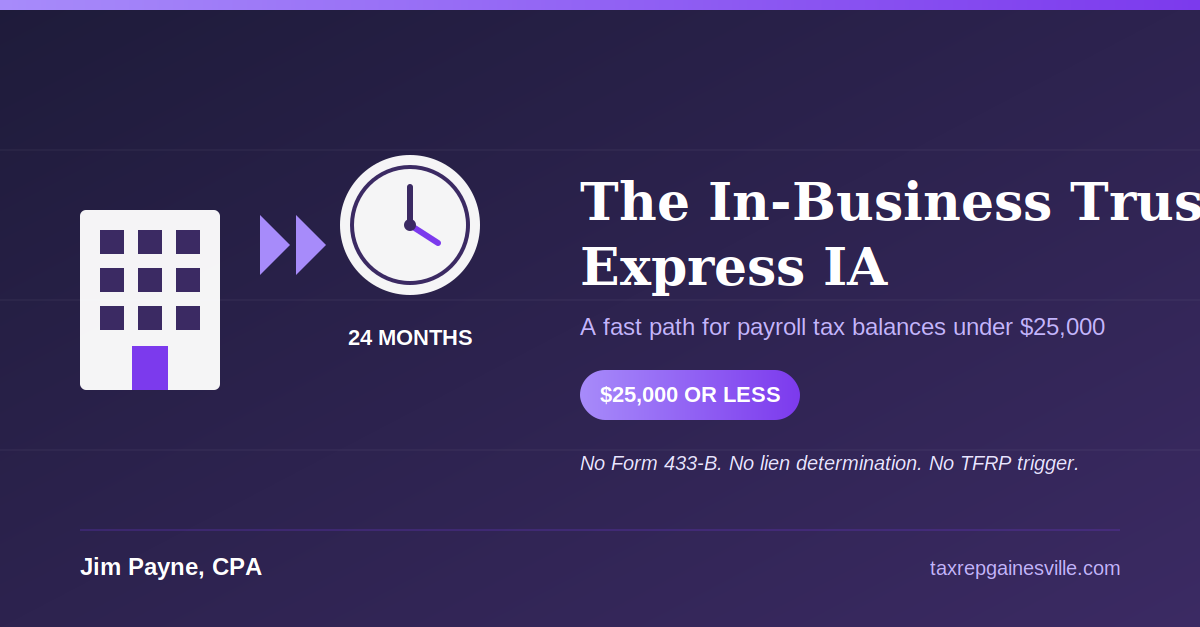

The In-Business Trust Fund Express Agreement

There is a separate streamlined track for operating businesses: the In-Business Trust Fund Express Installment Agreement, governed by IRM 5.14.5.3. This option is available to businesses that owe $25,000 or less in payroll tax liabilities (Form 941), are current on all deposit requirements, and can make full payments within 24 months or before the CSED. No CIS is required. Like the individual streamlined track, this agreement requires direct debit.

This is worth knowing because it gives compliant businesses a path to resolve a manageable payroll tax balance without the scrutiny of a full financial review — provided they act quickly before the balance grows past the threshold.

Which Track Is Your Client On?

The practical decision tree looks like this:

- Balance $10,000 or under, all returns filed, no prior IA in five years → Guaranteed IA, mandatory acceptance, no CIS

- Balance $10,001–$50,000, individual → Streamlined IA, no CIS, 72-month window, DDIA required above $25,000

- Balance over $50,000, individual or business → Non-Streamlined, full CIS required, IRS discretion on terms

- Operating business, payroll tax balance $25,000 or under, deposit-current → In-Business Trust Fund Express, no CIS, 24-month window

Knowing the track before you contact the IRS shapes every aspect of the representation — what forms to prepare, what documentation to gather, what payment figure to propose, and whether financial disclosure is even on the table.

If your client is already in an installment agreement and struggling to stay current, see my post on what happens when an IRS installment agreement defaults for the next steps. And if you're still weighing whether an IA is the right resolution strategy at all, our earlier post on when an installment agreement makes sense — and when it doesn't covers how to evaluate the alternatives.

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances