What Happens When the IRS Assigns Your Case to a Revenue Officer

This is a subtitle for your new post

Most IRS collection activity begins in the automated system. Notices are mailed, balances increase with penalties and interest, and the taxpayer is asked to resolve the account by making a payment or setting up a payment plan. In many cases, these matters are handled without direct contact from an IRS employee. It's even questionable whether or not a human being is in the process at all.

But sometimes the case moves beyond the automated system. When the IRS assigns a case to a Revenue Officer, the situation changes.

What a Revenue Officer Does

A Revenue Officer is an IRS employee responsible for collecting unpaid taxes through direct case management. Instead of relying on automated notices, the Revenue Officer personally reviews the account and determines how the liability should be resolved. Revenue Officers typically handle cases that involve larger balances, payroll tax liabilities, or situations where previous notices have not resulted in resolution.

Their responsibilities include:

- Contacting the taxpayer directly

- Gathering financial information

- Determining the taxpayer’s ability to pay

- Pursuing enforcement actions when necessary

The IRS describes this process in the Internal Revenue Manual under IRM 5.1 – Field Collection Procedures: https://www.irs.gov/irm/part5/irm_05-001

Contact From a Revenue Officer

When a Revenue Officer is assigned, the first contact is often a phone call, a letter, or, sometimes, an unannounced visit to the business or residence. The purpose of this contact is usually straightforward: to establish communication and begin gathering information about the taxpayer’s financial condition. This often leads to requests for documents such as bank statements, financial disclosures, or business records.

Financial Analysis Becomes Central

Once a Revenue Officer is involved, the focus usually shifts toward financial analysis.

The IRS will often request a financial statement—such as Form 433-A or Form 433-B—to determine what the taxpayer can realistically pay. Income, expenses, assets, and cash flow are evaluated to determine the appropriate resolution. This financial analysis often drives the case's eventual outcome.

Enforcement Authority

Revenue Officers also have the authority to pursue enforcement actions when necessary. This may include filing federal tax liens or issuing levies on wages, bank accounts, or other assets. However, enforcement is typically used after attempts to resolve the case through voluntary compliance.

Why Early Communication Matters

Assignment to a Revenue Officer does not mean enforcement is inevitable. In many cases, it simply means the IRS has determined the situation requires direct attention rather than automated notices. Responding promptly and understanding the financial realities of the case can often lead to a more structured resolution.

When a Revenue Officer becomes involved, the process becomes more direct—but it also becomes clearer. The IRS is now focused on understanding the situation and determining how the liability can realistically be resolved.

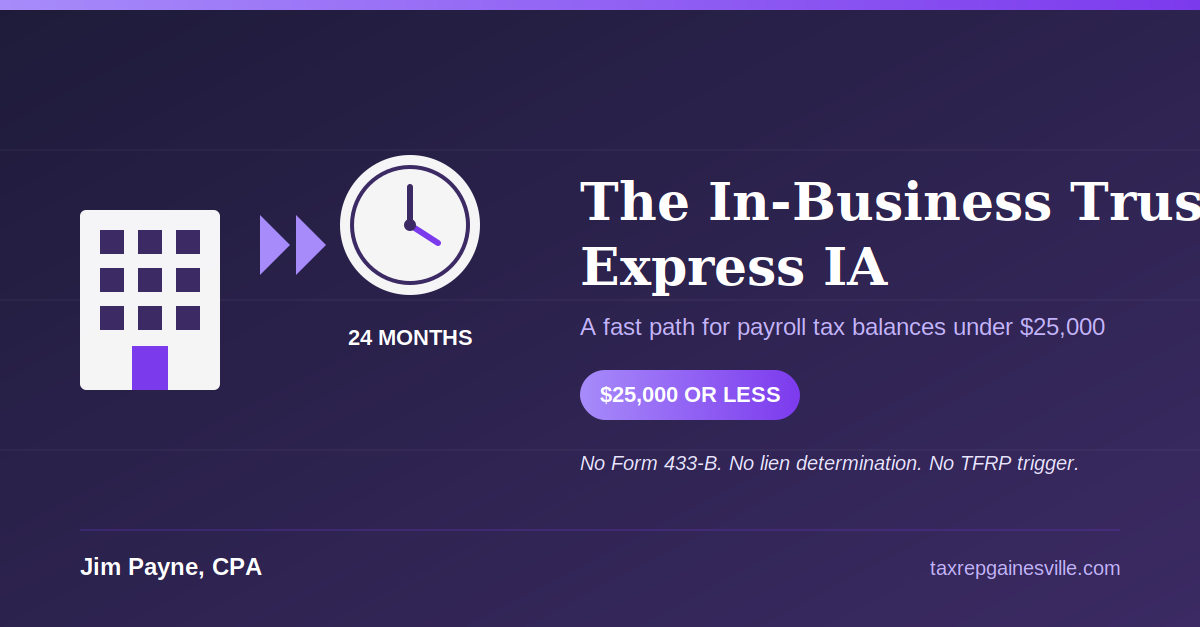

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances