IRS Levy: What the IRS Can Take and When

This is a subtitle for your new post

When the IRS uses the term "levy," it refers to the legal authority to seize property to collect unpaid taxes. A levy is one of the IRS’s most direct collection tools. It allows the government to seize assets or intercept payments that would otherwise go to the taxpayer.

However, levies do not happen without warning. They are part of a structured collection process that includes several required steps before enforcement begins.

What the IRS Can Levy

The IRS has broad authority to levy many types of property. Common examples include:

- Bank accounts

- Wages and salaries

- Accounts receivable

- Retirement income

- Rental income

- Other payments owed to the taxpayer

In some cases, the IRS may also seize and sell physical assets such as vehicles or business equipment, although this is less common.

The legal authority for levies is found in Internal Revenue Code §6331: https://www.law.cornell.edu/uscode/text/26/6331

Bank Levies and Wage Levies

Two of the most common types of levies are bank levies and wage levies.

- A bank levy freezes the funds in a bank account on the day the levy is received by the bank. The funds are typically held for 21 days before being sent to the IRS.

- A wage levy works differently. Instead of taking a single payment, the levy continues against each paycheck until the debt is resolved or the levy is released.

When the IRS Can Issue a Levy

Before issuing most levies, the IRS must follow specific procedural steps.

Generally, the IRS must:

- Assess the tax

- Send a notice and demand for payment

- Issue a Final Notice of Intent to Levy

- Allow 30 days for the taxpayer to request a Collection Due Process hearing

These requirements are established under Internal Revenue Code §6330: https://www.law.cornell.edu/uscode/text/26/6330

If the taxpayer requests a hearing within that 30-day window, collection activity is typically paused while the appeal is considered.

Levies Are Usually the Result of an Unresolved Case

Levies usually mean the IRS has been ignored. In most cases, the IRS has already sent several notices requesting payment or proposing ways to resolve the balance. When those notices go unanswered or the situation remains unresolved, the case eventually moves to enforcement.

A levy is often the point where the IRS concludes that voluntary resolution has not occurred and direct collection action is necessary. The earlier the situation is addressed, the more flexibility usually exists to resolve the matter without enforcement.

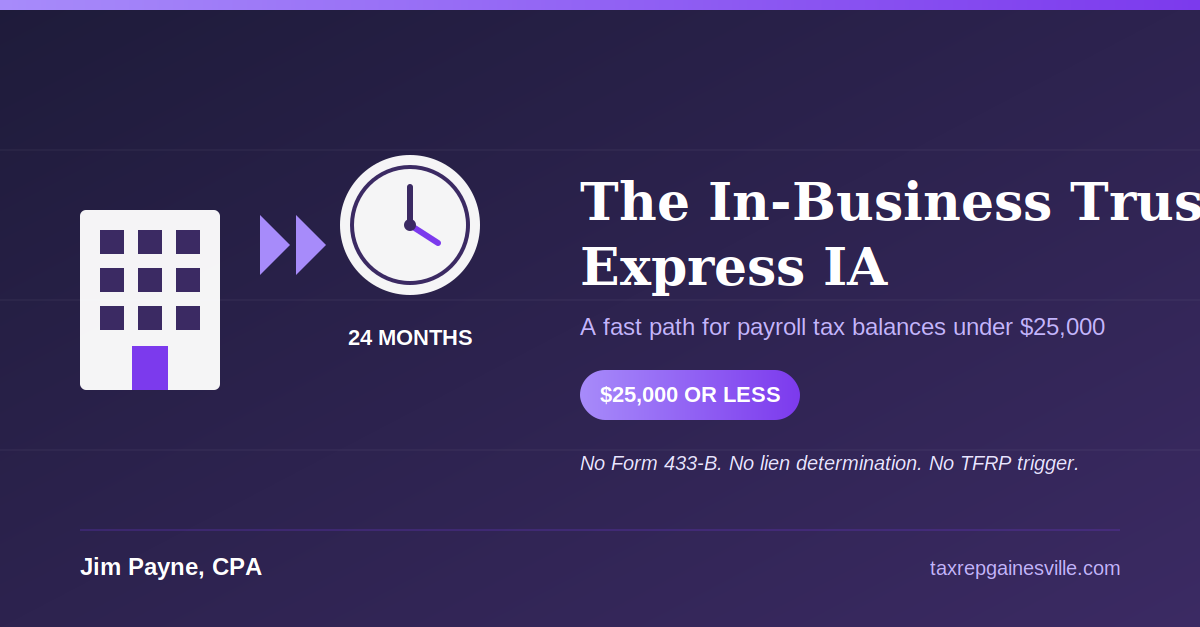

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances