What IRS Notices for Past Due Payroll Taxes Really Mean

This is a subtitle for your new post

Few IRS notices create more anxiety than those involving unpaid payroll taxes.

Most business owners don’t immediately assume the worst. They simply look at the notice and think, “This is another problem I don’t fully understand, and I’m not sure what to do next.” Payroll tax notices are technical, procedural, and often written in language that doesn’t clearly explain what stage the case is in.

Understanding what the notice actually represents is the first step toward controlling the situation.

Payroll Taxes Are Treated Differently

Payroll taxes are not the same as income taxes.

When an employer withholds federal income tax and FICA from employees’ wages, those funds are considered trust fund taxes. The employer is holding that money in trust for the government. Because of this, the IRS treats unpaid payroll taxes more seriously than most other business liabilities. This distinction is explained under Internal Revenue Code §6672, which authorizes the Trust Fund Recovery Penalty (TFRP): https://www.law.cornell.edu/uscode/text/26/6672

That statute allows the IRS to pursue certain individuals personally if trust fund taxes are not paid.

But receiving a notice does not mean that step has already happened.

Early Notices Are Part of a Sequence

Initial payroll tax notices are typically balance-due notices. They inform the business that deposits or filed returns reflect an unpaid amount. As the case progresses, notices become firmer. Eventually, the IRS may issue a Final Notice of Intent to Levy (Letter 1058 or LT11). This notice is required before most enforcement action can begin.

The IRS collection process is outlined in the Internal Revenue Manual under IRM 5.1.1 – Administrative Collection Process: https://www.irs.gov/irm/part5/irm_05-001-001

Each notice signals where the case sits in that process.

Revenue Officer Assignment Changes the Tone

If the payroll liability remains unresolved, the case may be assigned to a Revenue Officer.

At that point, the focus typically shifts from the business entity alone to identifying responsible individuals. This is where interviews, financial disclosures, and trust fund investigations may begin.

Not every payroll tax case results in a Trust Fund Recovery Penalty. But ignoring early notices increases the likelihood that the case escalates to that stage.

Why Timing Matters

Payroll tax problems rarely improve on their own.

However, escalation is procedural—not personal. The IRS follows the required steps before enforcement or a personal assessment occurs. Understanding those steps allows a business owner to act deliberately rather than react emotionally.

If you’re already dealing with payroll tax exposure, it’s important to understand where your case is in the sequence. The earlier the analysis begins, the more options typically remain available.

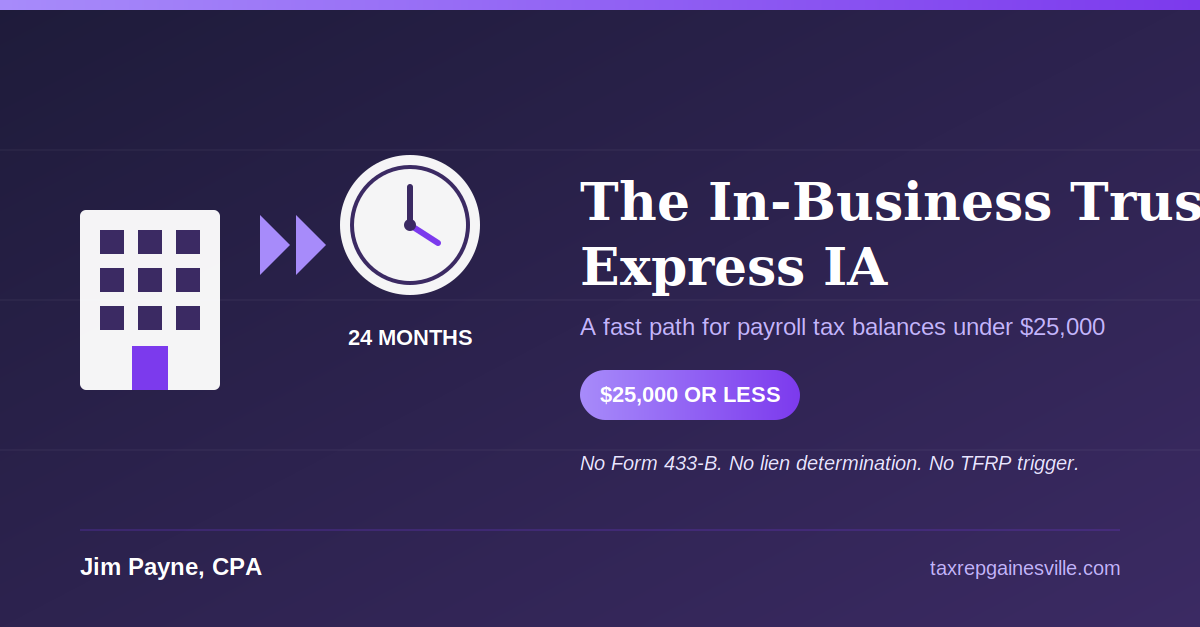

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances