Business Broke… But You Owe $50K+ in Payroll Taxes? Read This First.

This is a subtitle for your new post

First—take a breath. This situation is more common than you think.

Now the hard truth: Payroll taxes don’t go away just because your business closed. Why? Because part of that money (employee withholdings) was never yours to begin with. The IRS treats it differently—and much more aggressively.

Here’s what usually happens next:

- The IRS investigates who was “responsible.” They look at who controlled finances, signed checks, and made the decision not to pay the 'Trust Funds".

- They next assess a Trust Fund Recovery Penalty (TFRP) on the individuals whom they found responsible. This debt is PERSONAL—even if you had an LLC or corporation.

- Collections don’t stop just because the business is gone. They now use bank levies, wage garnishments, and liens on whatever assets the responsible persons might have.

But here’s what most people don’t realize: You still have options. Depending on your situation, you may be able to:

• Set up a payment plan based on what you can actually afford

• Qualify for Currently Not Collectible (CNC) status

• Challenge or reduce the penalty if responsibility is unclear

• In some cases, settle for less through an Offer in Compromise

The key is timing and strategy. What you DON’T want to do:

• Ignore IRS notices

• Assume the debt died with the business

• Wait until enforcement starts

Early action gives you more control—and more options. If you’re in this situation, start by understanding where you stand before reacting emotionally. The IRS has a process. And once you understand it, this becomes a lot more manageable.

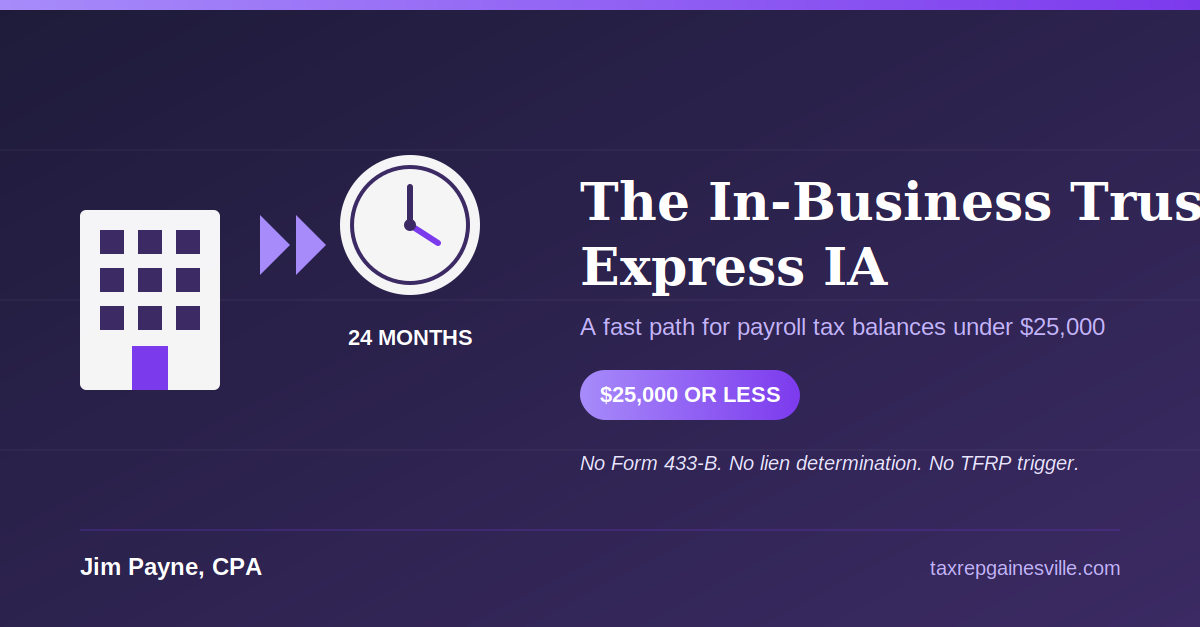

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances