Trust Fund Recovery Penalty: What CPAs Must Know Before the Form 4180 Interview

This is a subtitle for your new post

When a business falls behind on payroll taxes, the Revenue Officer's first priority is establishing personal liability — not resolving the company debt. By the time your client calls you, the IRS may have already begun building its case. Here is what the IRM requires the RO to prove, and where practitioners find the most leverage.

The Legal Standard Under IRM 5.7.3

The Trust Fund Recovery Penalty (TFRP) is authorized under IRC § 6672. Under IRM 5.7.3, the IRS must establish two independent elements before asserting it against an individual:

- Responsibility — the person had authority and control over the funds or the decision not to pay them.

- Willfulness — the person was aware the taxes were not being paid and either intentionally disregarded that obligation or acted with reckless disregard for it.

Responsibility is not tied to job title. The IRM instructs Revenue Officers to look at who actually controlled financial decisions: check-signing authority, access to banking, the ability to hire and fire, control over which creditors got paid. A minority shareholder with no check-signing authority is a very different case from a CFO who directed vendor payments while deferring payroll deposits.

Willfulness is satisfied under the IRM whenever a responsible person was aware of the unpaid taxes and used available funds to pay other creditors instead. This is where most assessments are sustained — the IRS doesn't need to show bad intent, only that your client knew and chose otherwise.

The Form 4180 Interview: Where Cases Are Won or Lost

IRM 5.7.4 governs the investigation process. The RO will request a Form 4180 (Report of Interview with Individual Relative to Trust Fund Recovery Penalty) interview with every potentially responsible person. This is not a friendly conversation.

The Form 4180 asks detailed questions about: who signed checks, who had bank access, who filed returns, who made the decision to pay other vendors, and whether the person knew taxes were delinquent. Answers given in this interview become part of the administrative record. If a client volunteers that they "knew taxes were overdue but had to keep the lights on," willfulness is effectively conceded.

Practitioner Guidance

Represent your client at the Form 4180 — or have a representative present before they respond to any IRS contact. IRM 5.7.3 makes clear that responsibility is fact-specific, and the factual record built during the investigation determines whether the penalty is asserted. Key defensive positions include:

- Documenting that the individual lacked actual financial authority (board resolutions, bank signature cards, organizational charts)

- Establishing that the individual made no affirmative decision to defer taxes — i.e., was not aware of delinquency until after the fact

- Where multiple potentially responsible persons exist, the IRS may assert the penalty against all of them, but the total tax is collected only once (IRM 5.19.14). This creates negotiating dynamics.

The Letter 1153 and the 60-Day Window

Once the RO recommends assessment, IRS issues Letter 1153, the Proposed Trust Fund Recovery Penalty notice. The client has 60 days to file a written protest. Missing this window results in automatic assessment, at which point the liability becomes a personal debt — not dischargeable in bankruptcy, collectible against personal assets, and subject to the full IRS collection arsenal including liens, levies, and wage garnishment.

If the protest is filed timely, the case transfers to Appeals. IRM 5.7.6 governs protest processing and the subsequent Appeals referral.

When to Call a Specialist

TFRP cases require a practitioner who can evaluate the Form 4180 record, assess the strength of the responsibility and willfulness arguments, manage protest strategy with Appeals, and — if the penalty is ultimately assessed — pivot to collection alternatives including installment agreements and, in limited cases, Offers in Compromise.

If your business client has received a Notice of Federal Tax Lien related to payroll taxes, or if a Revenue Officer has begun contacting company personnel about a Form 4180 interview, the time to involve a tax representation specialist is now — before positions are locked in.

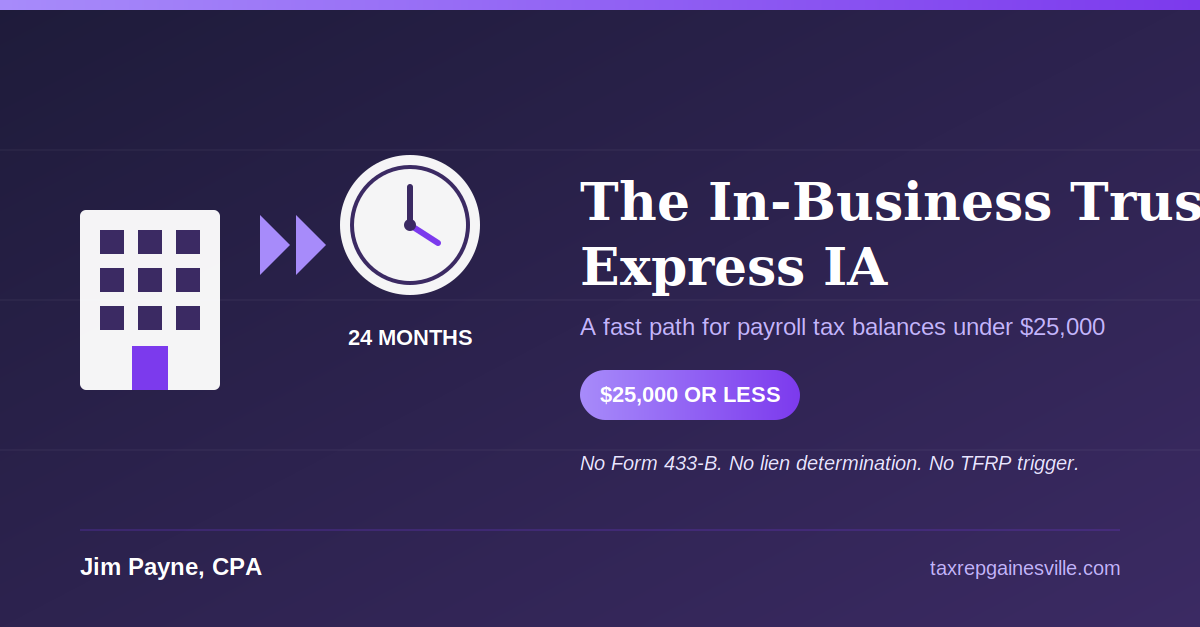

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances