Business Installment Agreements: What Practitioners Should Know Before Referring a Client

This is a subtitle for your new post

When an individual taxpayer owes the IRS, the installment agreement process is relatively straightforward. A business client is a different matter. The Form 433-B, Collection Information Statement for Businesses, introduces a level of financial scrutiny that catches many practitioners off guard — and a poorly prepared financial statement can stall or kill an agreement that should have been approved.

Here's what to understand before you refer a business client with an IRS balance.

The IA landscape for business accounts

IRM 5.14.7 governs installment agreements for Business Master File accounts, which primarily cover entities with Employer Identification Numbers. These procedures apply to balance due accounts, unassessed liabilities on secured returns, and liabilities in notice status — but only when the taxpayer has the ability to pay both current operating expenses and delinquent taxes. That last condition is critical: the IRS will not approve a business installment agreement for an entity that can't demonstrate it can stay current going forward. irs

For business accounts, three types of agreements come into play depending on the balance and the nature of the liability.

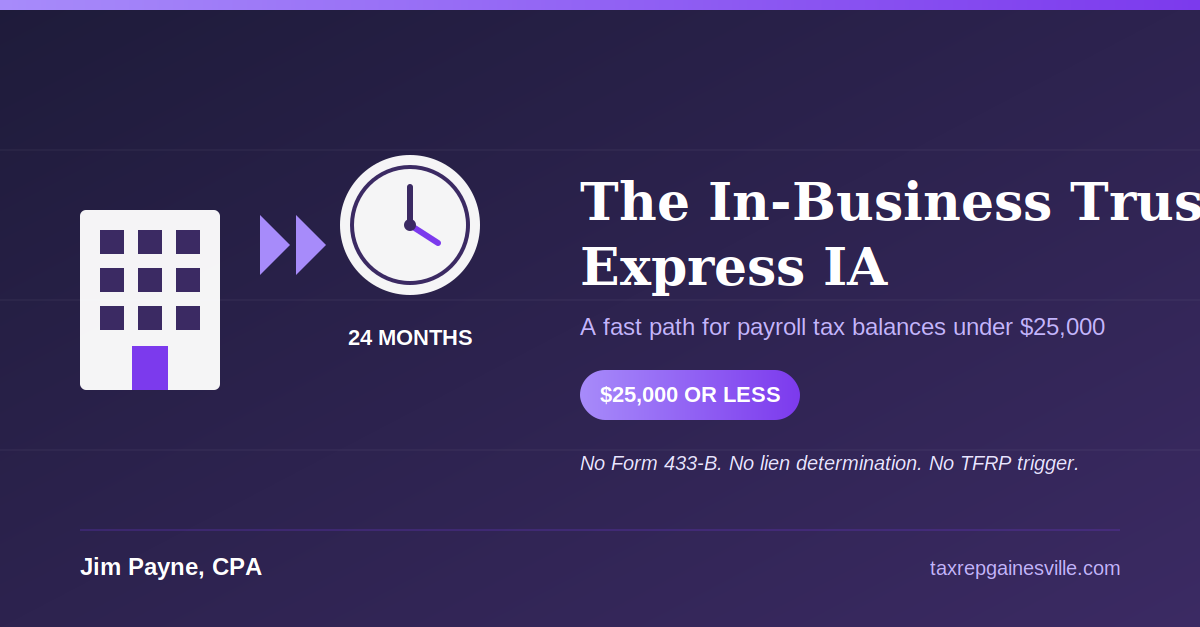

In-Business Trust Fund Express agreements

The IBTF Express IA is available when the unpaid assessment balance — the SUMRY balance — is $25,000 or less. A taxpayer with a balance above $25,000 can qualify if they pay the liability down to $25,000 or below before the agreement is granted, but a lump-sum payment made solely to reach that threshold at the time of granting is not permitted.

The IBTF Express is the path of least resistance for qualifying business clients. No full financial statement is required, and under qualifying conditions, the IRS will generally defer assessment of the Trust Fund Recovery Penalty. If your client is close to the threshold, it's worth discussing whether paying down to $25,000 makes sense before pursuing any agreement.

When financial analysis is required

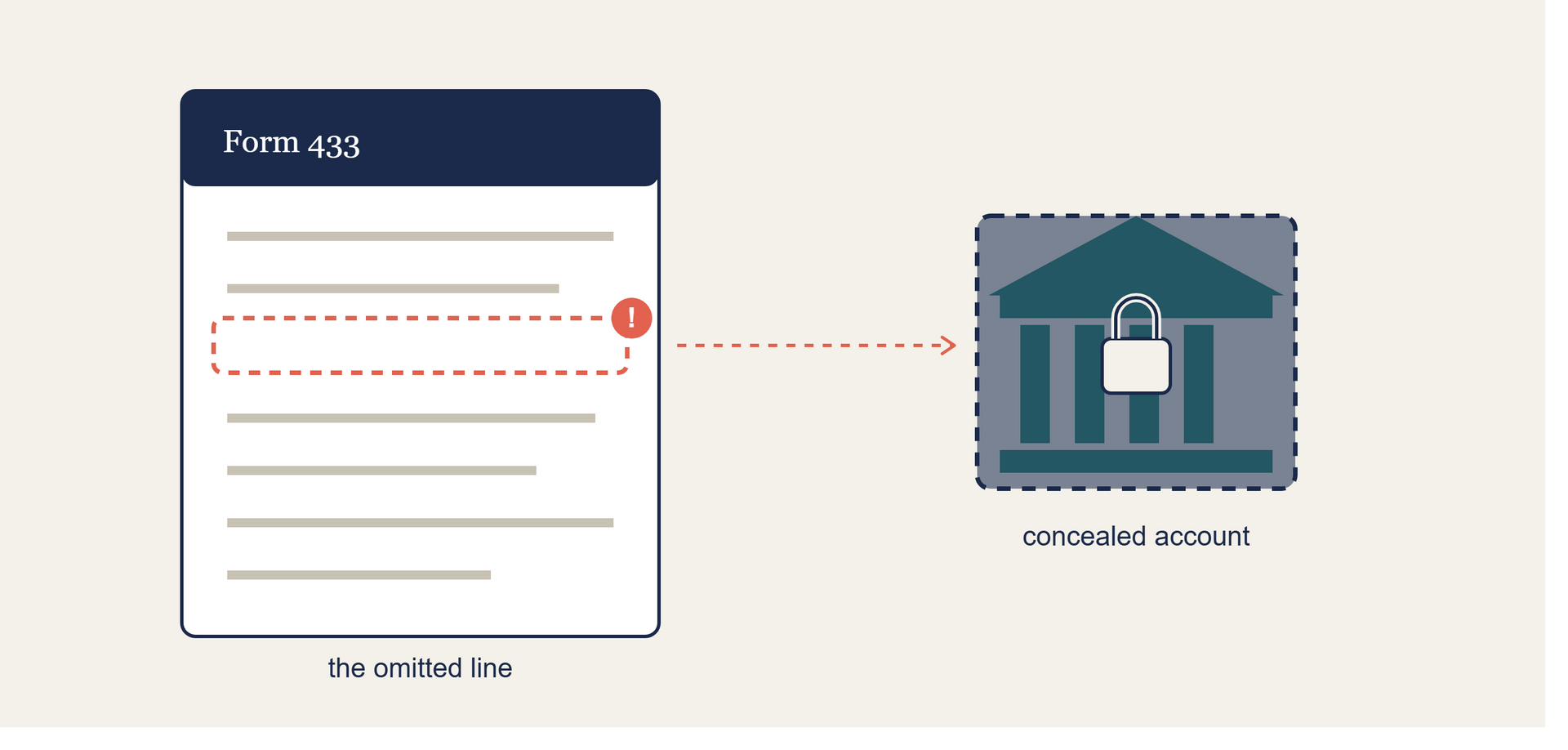

Once the balance exceeds the IBTF Express threshold, Form 433-B must be completed to determine the taxpayer's ability to pay. The IRS will compare current-year income information to the income reported on the last-filed return and verify the assets disclosed in the financial statement. If current-year income has decreased 20% or more from the last filed return, or if assets are identified that were not disclosed on the financial statement, the IRS will require the discrepancy to be explained and resolved before proceeding.

This is where most referrals arrive with problems. Common 433-B pitfalls I see:

Assets understated or omitted. Business owners frequently underreport accounts receivable, equipment value, or cash on hand. The IRS cross-checks against IDRS and filed returns. An inconsistency doesn't just delay the case — it signals bad faith and can result in rejection.

Income overstated as expense. Pass-through income, officer compensation, and distributions are often mischaracterized. The IRM requires the IRS to analyze the business's actual ability to pay, not the picture the taxpayer prefers to present.

Compliance not established first. Before an installment agreement can be approved, the taxpayer must be in compliance with filing requirements. A NFTL determination must also be made on accounts that don't qualify for streamlined or IBTF Express processing. Arriving at a resolution negotiation with unfiled returns is a non-starter. Every open return period needs to be filed before the 433-B is submitted.

Current deposits not current. For any business with ongoing payroll tax obligations, the IRS will verify that federal tax deposits are current before agreeing to a payment plan on back liabilities. A business that is still accruing new 941 debt will not be approved for an installment agreement on old 941 debt.

The TFRP question

Because an IBTF installment agreement will not fully satisfy the liability in most cases, the Trust Fund Recovery Penalty will typically be assessed. The IRS requires the revenue officer to ensure that the Assessment Statute Expiration Date is extended on accounts where the trust fund balance is below the threshold requiring investigation, and may request a signature on Form 2750, Waiver Extending Statutory Period for Assessment of Trust Fund Recovery Penalty.

This matters for your attorney clients in particular. If the business has responsible persons — officers, partners, or others who control payroll tax decisions — the TFRP exposure follows those individuals personally. That's a separate liability and, potentially, a separate representation matter.

Partial Pay Installment Agreements

When a taxpayer can make payments but cannot fully pay all balance-due accounts, a Partial Payment Installment Agreement may be considered. Under IRM 5.14.2, a PPIA is structured so that payments are made based on the taxpayer's actual ability to pay, with the remaining balance potentially expiring at the Collection Statute Expiration Date (CSED) — typically 10 years from assessment under IRC §6502. A PPIA requires the same 433-B financial analysis as a full-pay agreement, and the IRS will conduct periodic reviews of the taxpayer's financial condition and may increase payments if the taxpayer's financial condition improves.

The referral decision

A business installment agreement involving 941 debt, a balance over $25,000, or responsible-person TFRP exposure is a specialist matter. The financial statement preparation alone requires knowledge of IRS-allowable expense standards, asset valuation methodologies, and how the IRS will treat pass-through income — none of which is intuitive.

If your business client has an outstanding IRS balance and no resolution in place, I'm glad to review the situation and advise on the right approach before the IRS moves to enforced collection.

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances