Why Timing Matters in Discharging IRS Debt in Bankruptcy

This is a subtitle for your new post

Bankruptcy can eliminate certain types of IRS debt. But not all tax debt qualifies, and when it does often depends on timing. In many cases, the difference between dischargeable and non-dischargeable tax debt is not the amount owed. It is whether specific timing requirements have been met before the bankruptcy is filed.

Not All Tax Debt Can Be Discharged

The starting point is understanding that only certain income tax liabilities may be discharged in bankruptcy. Other types of tax debt, such as payroll taxes or more recent liabilities, generally are not dischargeable. Even for income taxes, additional requirements must be satisfied before the debt can be eliminated.

The Key Timing Rules

Three timing rules usually control whether income tax debt may be discharged in bankruptcy.

- The first is the 3-year rule. The tax return must have been due at least three years before the bankruptcy filing date.

- The second is the 2-year rule. The tax return must have been filed at least two years before the bankruptcy case is filed.

- The third is the 240-day rule. The IRS must have assessed the tax at least 240 days before the bankruptcy filing.

These rules work together. In most cases, all of them must be met before the tax debt is eligible for discharge.

Why Filing Too Early Can Be a Mistake

Some taxpayers begin considering bankruptcy as soon as IRS collection pressure increases.

The problem is that filing too early can prevent otherwise dischargeable tax debt from being eliminated. If the 3-year, 2-year, or 240-day requirements have not been met, the tax debt may survive the bankruptcy.

That means the taxpayer goes through the bankruptcy process but still owes the IRS afterward.

In many cases, timing—not the type of debt—is what changes the result.

Waiting Has Risks Too

Waiting is not always harmless. While the taxpayer is waiting for those timing rules to be satisfied, the IRS may continue its collection activity. Liens may be filed, and in some cases, levies may be imposed. This is why bankruptcy strategy is not just a question of whether to file. It is also a question of when to file to produce the best result.

Timing and Strategy Have to Work Together

As with other IRS matters, bankruptcy should not be evaluated in isolation. Financial condition still matters. The taxpayer’s overall debt, cash flow, and ability to pay all affect whether bankruptcy makes sense. But timing adds a second layer of analysis.

A case that does not work today may become viable later—not because the financials changed, but because the timing requirements were finally met.

The Real Question

In bankruptcy cases involving IRS debt, the real issue is rarely just whether bankruptcy is an option.

The real question is whether the timing is right. When it is, bankruptcy may eliminate tax debt that would otherwise remain. When it is not, the IRS may still be waiting on the other side of the case.

In these situations, timing can be the difference between a strategy that works and one that leaves the tax debt in place.

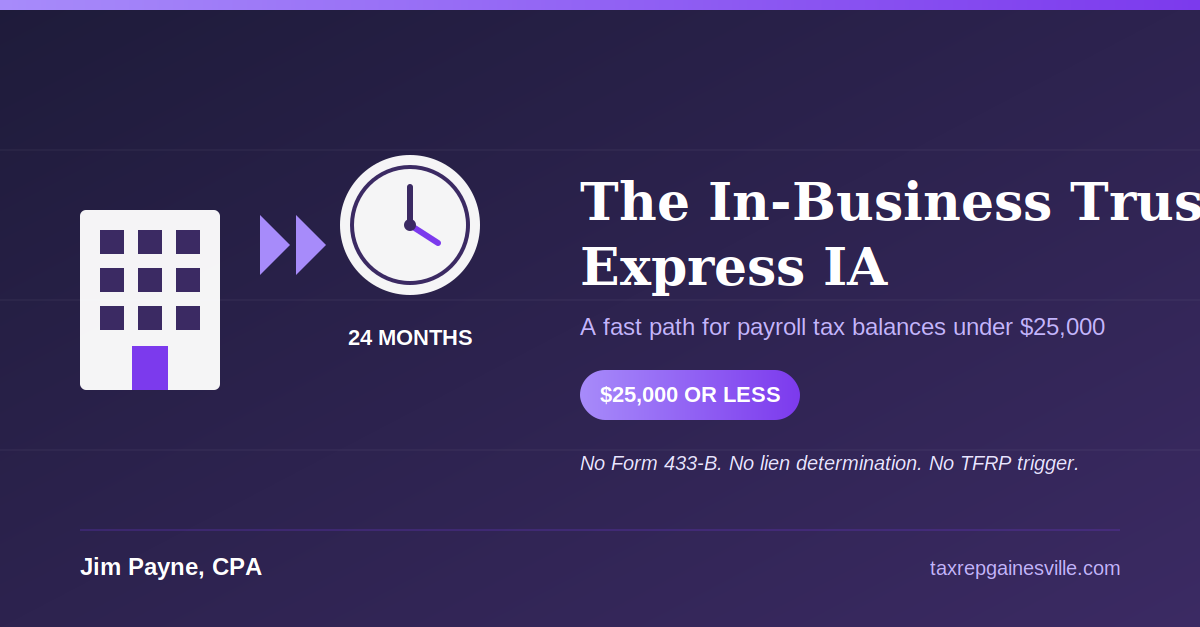

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances