Offer in Compromise for Business Clients: Why the RCP Calculation — Not the IRS Prequalifier — Controls the Outcome

This is a subtitle for your new post

The Offer in Compromise is the most misunderstood program in IRS collections. Consumer advertising has trained clients to believe any back tax debt can be settled for pennies on the dollar. The IRM tells a different story — and practitioners who understand the actual mechanics can both serve their clients better and provide more credible referrals.

The Three Grounds for an OIC

Under IRC § 7122 and IRM 5.8.1, the IRS may accept an OIC on three grounds:

- Doubt as to Collectibility (DATC) — the most common; the taxpayer cannot pay the full liability within the remaining collection statute

- Doubt as to Liability (DATL) — the underlying assessment itself is disputed

- Effective Tax Administration (ETA) — full payment is technically possible but would create economic hardship or be fundamentally unfair given the taxpayer's circumstances

Business clients typically present under DATC. ETA offers for businesses are rare and require a compelling showing beyond mere inability to pay.

What Actually Drives the DATC Determination: Reasonable Collection Potential

IRM 5.8.5 governs the financial analysis. The IRS evaluates every DATC offer by calculating Reasonable Collection Potential (RCP):

RCP = Net Realizable Value of Assets + Future Income Component

Net Realizable Value is the quick-sale value of the taxpayer's assets (generally 80% of fair market value for most assets) minus secured debt. For business clients, this includes accounts receivable, equipment, inventory, and — critically — equity in real property. The IRS will identify assets your client may not think to list.

Future Income Component is where most business-owner offers are mispriced. For a lump-sum (cash) offer, the IRS multiplies monthly disposable income by 12. For a deferred (periodic payment) offer, the multiplier is 24. Disposable income is calculated using IRS National and Local Standards for allowable expenses — not the client's actual spending — against income from all sources.

The IRS will accept an offer at or above RCP. It will reject an offer below RCP unless the numbers can be legitimately reduced.

Common Calculation Errors in Self-Prepared Offers

The Pre-Qualifier Tool on IRS.gov uses simplified inputs and routinely suggests eligibility for clients whose actual RCP — once the financial statements are properly developed — exceeds the amount they could realistically offer. The consequences of a mispriced offer: the 20% nonrefundable deposit on lump-sum offers is forfeited, the CSED is tolled during the entire investigation period, and collection activity resumes immediately upon rejection.

Areas where practitioners frequently find legitimate RCP reduction opportunities:

- Dissipated assets: Under IRM 5.8.5, the IRS can add back assets transferred within the prior five years that reduced collectibility. Knowing what the RO will include before submitting avoids surprise rejections.

- Business entity vs. individual liability: A business OIC on Form 433-B and an individual OIC on Form 433-A are separate submissions with separate RCP calculations. In TFRP cases, this creates a layered strategy — resolving the business liability first can reduce or eliminate the individual exposure.

- Expense allowances: The IRM allows national and local standard amounts without documentation, but conditional expenses (above-standard housing, vehicle expenses, health costs) require substantiation. Practitioners who document these correctly reduce the disposable income figure and lower RCP.

- CSED timing: The collection statute expires 10 years from assessment. Where significant CSED time has run, the future income multiplier may produce a lower RCP than the IRS initially calculates — or currently not collectible (CNC) status may be a stronger alternative than an OIC.

When OIC Is Not the Right Answer

For business clients with ongoing operations and improving income, the IRS will calculate future income based on projected earnings — not current distress. A client whose business is recovering may face an RCP that reflects the ability to pay through an installment agreement. In those cases, a properly structured installment agreement or PPIA (Partial Pay Installment Agreement) under IRM 5.14.2 may resolve the debt at less total cost than an OIC attempt.

The OIC program is also not available while the taxpayer is in open bankruptcy, has unfiled returns, or has an unresolved open audit — IRM 5.8.3 requires all returns filed and all estimated tax current as a processability requirement.

The Referral Question

When a client asks their CPA whether they "qualify" for an OIC, the honest answer is that qualification is less important than whether the offer can be priced at a number the client can actually pay. That requires a full RCP analysis before the Form 656 is submitted. If the analysis suggests a viable offer, the case warrants representation by a practitioner who handles financial statement development, manages contact with the Revenue Officer during the investigation, and negotiates at Appeals if the offer is rejected.

That is exactly the kind of case where a referral to a tax representation specialist adds value — for your client, and for the integrity of your practice.

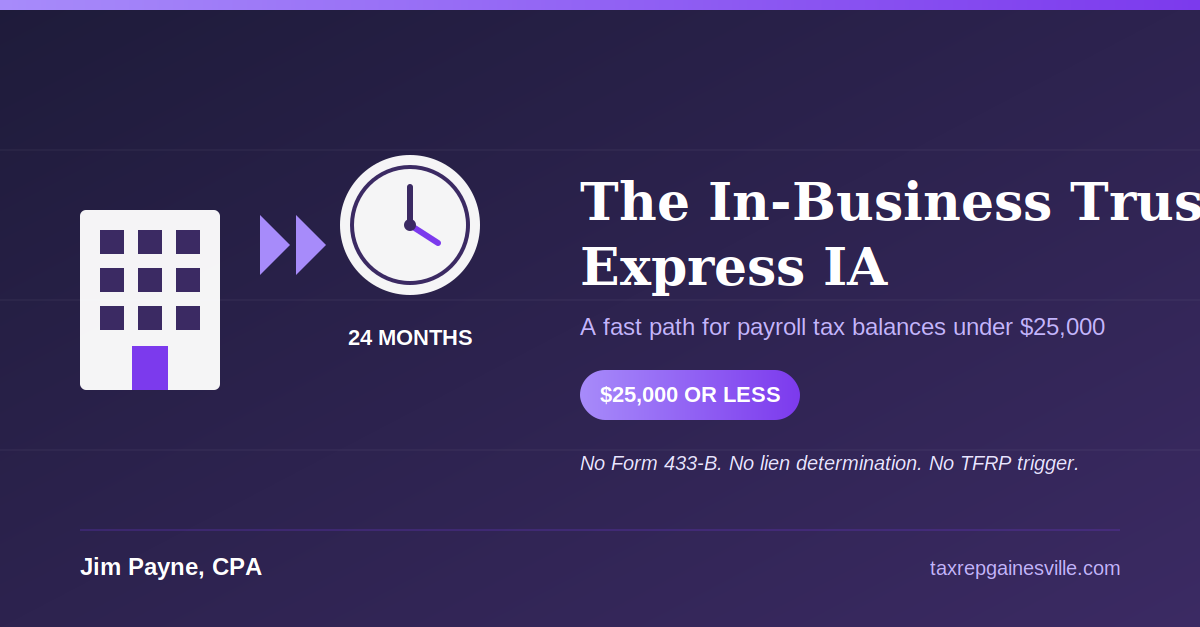

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances