Why IRS Strategy Starts With a Financial Analysis

This is a subtitle for your new post

People often call me with the same question: “Should I or can I get a payment plan?”

My answer is almost always the same. “I don’t know.”

That response sometimes surprises people. They assume a professional should immediately know which option makes sense. But without a financial analysis, there is no data to work from—and without data, any advice would be a guess.

Strategy Without Data Is Just Guessing

A payment plan might be the right move. Or it might be the worst possible choice.

Until I understand someone’s income, expenses, assets, cash flow, and filing status, there is no way to responsibly suggest a strategy. The IRS does not decide cases based on intent or effort. It decides them based on numbers.

Without those numbers, there is no strategy—only motion.

The IRS Bases Options on Financial Reality

Every meaningful IRS option depends on a financial picture.

Payment plans are approved based on the ability to pay. Hardship status depends on whether basic living expenses can be met. Settlement options depend on what the IRS believes it can collect over time.

Two people can owe the same amount and face very different outcomes because their financial realities are different. That’s why asking “should I get a payment plan?” without context is like asking whether you should refinance without knowing your income or credit.

Why Payment Plans Are Often Chosen Too Quickly

Payment plans feel safe. They relieve immediate pressure and create a sense of progress.

But that doesn’t mean they’re always the right first step.

In some cases, a payment plan locks someone into an obligation they can’t sustain. In others, it eliminates leverage or delays addressing a deeper compliance problem. Without analyzing the numbers, it’s impossible to know whether a payment plan fits—or whether it will quietly fail later.

Financial Analysis Comes Before Any Real Advice

A financial analysis answers the questions that actually matter:

- What does the IRS think you can afford?

- What does your cash flow realistically support?

- Where is the case in the IRS system right now?

Only after those answers are clear does it make sense to talk about strategy. Anything before that is speculation.

Strategy Is About Alignment, Not Optimism

A good IRS strategy aligns financial reality with IRS rules and timing.

It doesn’t chase the most appealing option. It chooses the option that fits the facts. That requires discipline, not optimism.

When someone asks me whether they should get a payment plan, my first answer has to be “I don’t know.” The second answer is more useful: “Let’s look at the numbers first.”

Because without a financial analysis, there is no strategy—only hope. Hope is not a plan when dealing with the IRS.

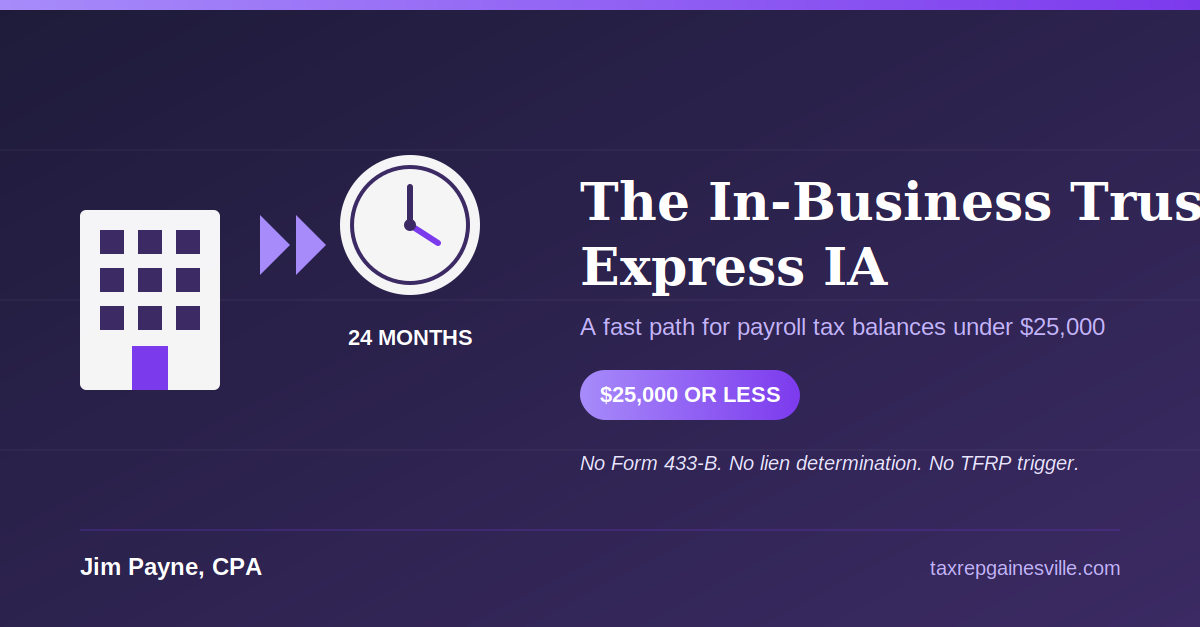

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances