Why the IRS Prefers Bank Levies Over Everything Else

This is a subtitle for your new post

When people worry about IRS enforcement, they often picture property seizures or dramatic actions.

In reality, the IRS usually starts with something far simpler: a bank levy.

That choice isn’t accidental. It reflects how the IRS thinks about efficiency, control, and results.

Bank Levies Are Administratively Simple

From the IRS’s perspective, a bank levy is one of the easiest enforcement tools available.

Once required notices have been issued, the IRS can levy a bank account without going to court. There is no lawsuit, no judge, and no waiting for approval. The levy is issued directly to the bank, and the process follows a predictable timeline.

Compared to other enforcement options, this simplicity matters. The IRS is managing millions of accounts. Tools that are fast and standardized get used first.

Cash Is Easier Than Property

Cash on deposit is already liquid. There is no need to value it, store it, insure it, or sell it.

When the IRS levies a bank account, it captures what is there at that moment, subject to the required holding period. That makes the outcome relatively certain. By contrast, seizing and selling property involves costs, delays, and risk that the sale will not meaningfully reduce the debt.

The IRS is a tax collector, not a liquidation business. Cash requires the least effort.

Bank Levies Send a Strong Signal

A bank levy is not just about collecting money. It is also a message.

From the IRS’s standpoint, a bank levy tests whether the taxpayer will engage. It often prompts a response when letters and notices have not. That response—whether it is communication, payment, or a request for resolution—gives the IRS information about how the case is likely to proceed.

In that sense, a bank levy is both a collection tool and a compliance tool.

Wage Levies Come Next, Not First

Many people assume wage levies are the IRS’s default enforcement option. They aren’t.

Wage levies are ongoing and effective, but they require employer involvement and long-term monitoring. Bank levies, by contrast, are one-time actions that can be repeated if necessary and require less follow-up.

That makes bank levies a natural first step when enforcement escalates.

Property Seizures Are Rare for a Reason

Although the IRS has the authority to seize vehicles, equipment, and even real estate, those actions are uncommon.

Property seizures require additional approvals and careful analysis to determine whether the seizure will produce meaningful results after costs and complications. If an asset produces income, the IRS usually prefers to levy the income rather than take the asset itself.

Bank accounts avoid those issues entirely.

What a Bank Levy Really Tells You

When the IRS issues a bank levy, it is not acting randomly or emotionally. It is choosing the tool that is easiest to deploy, easiest to manage, and most likely to produce a response.

Understanding that logic matters.

A bank levy doesn’t mean the IRS is out of options. It means the case has reached a point where voluntary compliance has failed, and the IRS is applying pressure in the most efficient way it knows how.

For taxpayers, recognizing why bank levies come first helps turn enforcement from something mysterious into something predictable—and predictability is often the first step toward regaining control.

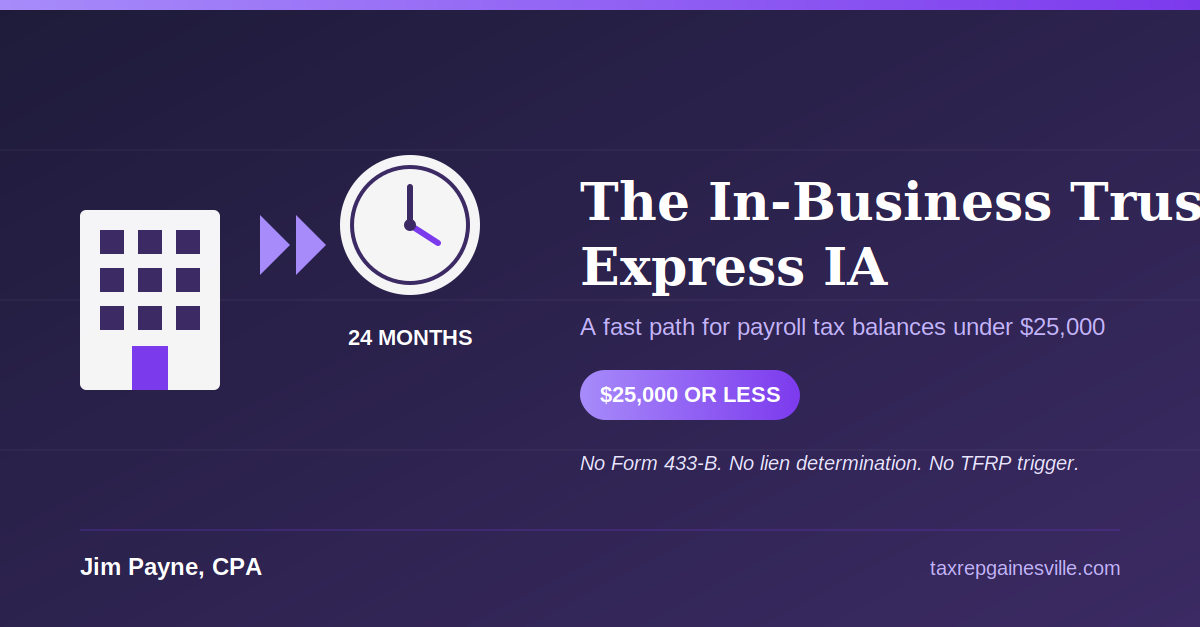

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances