When IRS Letters Stop Being Informational and Start Being Dangerous

This is a subtitle for your new post

Most IRS letters are not emergencies.

Early notices are informational. They confirm a balance, request a return, or explain a change. They can usually be handled with time, planning, and measured responses.

The problem is that many people assume all IRS letters are the same.

They aren’t.

At some point, IRS correspondence stops being about information and becomes about enforcement. The language changes. Deadlines become firmer. The consequences of inaction become real.

Early Letters Explain, Later Letters Warn

In the beginning, IRS letters tend to be explanatory. They describe what the IRS believes is owed or missing and invite a response. These notices often come in pairs or sequences, and missing one usually triggers another.

Because nothing immediate happens, people learn the wrong lesson: that IRS letters can be ignored safely.

That lesson eventually becomes expensive.

Enforcement Letters Are About Action, Not Awareness

As a case progresses, the tone shifts. Words like “intent,” “final,” and “levy” begin to appear. These letters are not asking for information. They are documenting that the IRS has met its notice requirements and is preparing to act.

By the time these letters arrive, the IRS has usually already tried softer approaches.

Ignoring them doesn’t pause the process. It accelerates it.

Deadlines Matter More Than Balances

One of the most common mistakes is focusing on how much is owed instead of where the case is in the IRS system.

Two taxpayers can owe the same amount and face completely different risks depending on which letters they’ve received and which deadlines have passed. Enforcement is driven by timing and compliance, not just dollars.

Once certain deadlines expire, options narrow. Some relief paths become harder or disappear altogether.

Why This Is the Wrong Time to Guess

When IRS letters reach the enforcement stage, guessing is dangerous.

Generic advice stops working because eligibility for options now depends on facts: filing status, assessment dates, enforcement posture, financial capacity, and prior history with the IRS. Online checklists can’t account for those variables.

This is usually the point where people realize they don’t need more information — they need clarity.

When a Situation Review Becomes Necessary

When IRS letters stop being informational, the right question is no longer “What does this letter mean?” It’s “What options still exist, given where my case is right now?”

Answering that requires looking at the whole picture: what’s filed, what’s assessed, what stage collections are in, and what the numbers actually support.

That’s why structured IRS situation reviews exist in the first place. They replace assumptions with facts and help people understand which paths are still open — before enforcement makes the decision for them.

IRS letters don’t become dangerous all at once. They become dangerous when they’re ignored for too long.

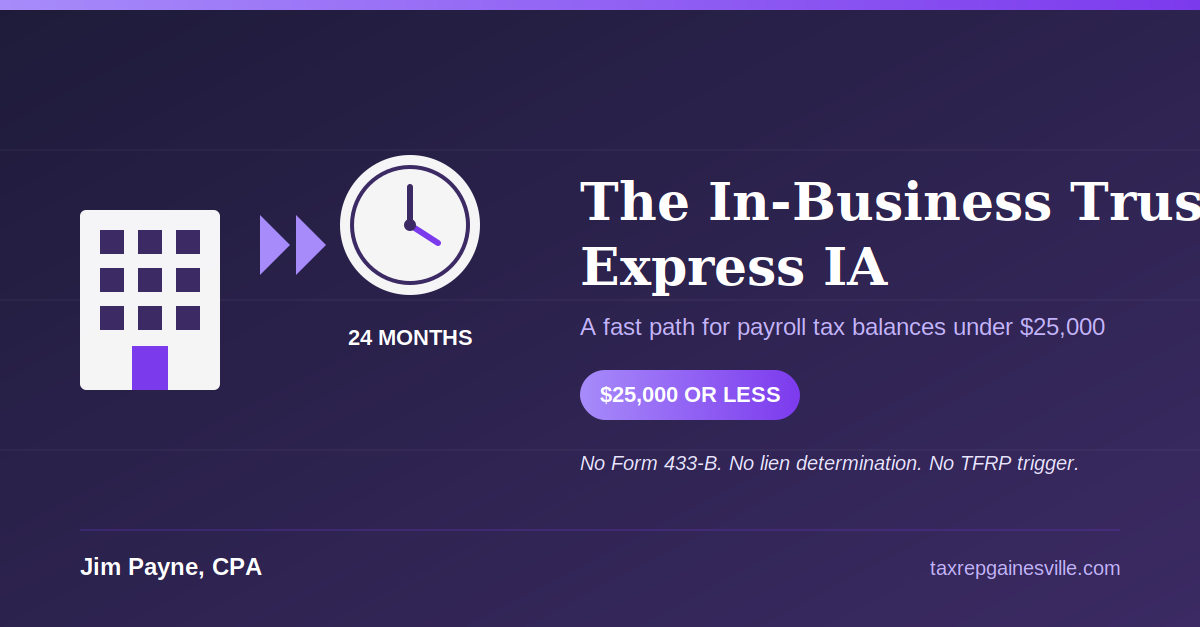

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances