Why Filing Early Matters When You’re Headed Toward IRS Representation

This is a subtitle for your new post

When people are behind with the IRS, “filing early” isn’t about being organized. It’s about leverage.

The IRS cares about one thing before it will take most resolution requests seriously: compliance. If required returns aren’t filed, the IRS can treat you as noncompliant and keep the case in enforcement mode. Filing early is how you prove you’re back on the right side of the line.

It also affects what can be addressed in a resolution.

If you’re considering an Offer in Compromise (OIC) or any structured resolution, the IRS generally needs the tax to be properly reported (and in many cases processed/assessed) so the liability is defined and can be included in the overall picture. Early filing gives your representative a cleaner, faster path to build a complete case instead of arguing about missing years while enforcement continues.

There’s another practical reason to file early: it prevents the IRS from filling in the blanks for you. When a return isn’t filed, the IRS can create a substitute assessment using only third-party income data—typically the worst possible version of your return because deductions and credits aren’t included.

But here’s the twist that trips people up: early filing does not necessarily mean filing immediately.

If your income is messy—multiple 1099s, brokerage activity, gig work, retirement distributions—accuracy matters. And the IRS does not make all third-party income data visible right away. The IRS’s Wage & Income transcript (the transcript that aggregates W-2s and 1099s) may not be complete early in the season and, depending on access method, often isn’t available until late May.

That’s where an extension becomes a smart compliance tool. Filing an extension avoids the failure-to-file problem while giving you time to reconcile missing or incorrect 1099s and file a return you can stand behind. (An extension doesn’t extend the time to pay, but it can prevent a bad return from creating a second problem.)

Bottom line: file early when you can file right—and when you can’t, file an extension early so compliance is established while the numbers get properly reconciled.

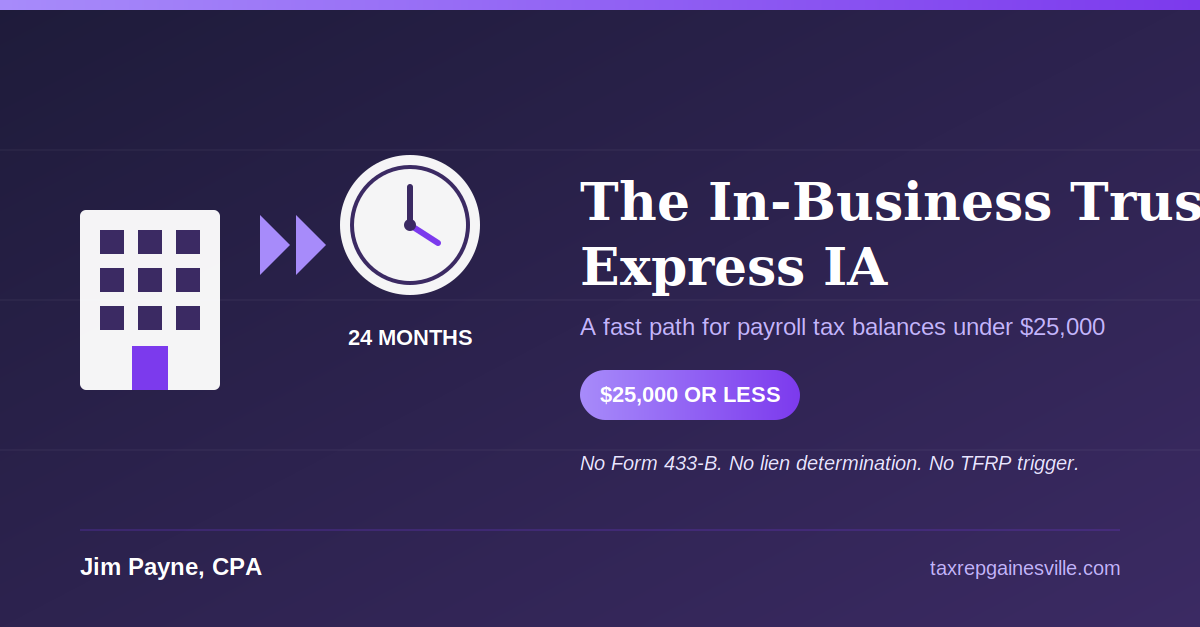

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances