When to Use a Doubt as to Liability Offer in Compromise (DATL OIC)

When most people think of settling a tax debt with the Internal Revenue Service, they picture the classic “pennies‑on‑the‑dollar” deal — formally an Offer in Compromise (OIC). But not all OICs are about being broke. Sometimes, the issue isn’t your ability to pay — it’s whether you even owe the tax at all.

That’s where a Doubt as to Liability Offer in Compromise (DATL OIC) comes in.

If you believe the IRS assessed tax you don’t actually owe, this special type of OIC gives you a path to dispute the debt without going through lengthy litigation or IRS appeals. But it’s not for everyone — and timing is everything.

What is a DATL OIC?

A Doubt as to Liability OIC is grounded in the notion that you shouldn’t be liable for all (or part) of the tax debt the IRS says you owe. This can arise from an error in the assessment, missing information, or a disagreement about how the tax law was applied.

According to IRM IRM 8.23.7: “Doubt as to liability exists when there is a genuine dispute as to the existence or amount of the correct tax debt under the law.”

IRS+2IRS+2

Additionally, IRM IRM 5.19.24 further details how DATL offers are processed.

IRS

Unlike the more common Doubt as to Collectibility (DATC) OICs, a DATL doesn’t focus on your ability to pay — instead, it focuses on whether the IRS got the tax right.

When is it the Right Time to Use One?

Here are some scenarios where a DATL OIC might be a smart option:

1. You Missed the Window to Dispute the Tax

Maybe you moved and missed your audit or appeal deadline. A DATL lets you challenge the assessment after the fact.

2. You Have New Evidence or Facts That Weren’t Considered

For example: if you discover additional documentation that was not available during the audit, a DATL may allow you to present it.

3. You Believe the IRS Assessed the Wrong Taxpayer or Applied the Law Incorrectly

If there’s a misidentification, mathematical mistake, or legal misapplication, you might qualify.

4. You Want to Avoid the Cost and Time of Litigation

Going to court can be expensive and time‑consuming. A DATL offers a more efficient path, when the issue is liability, not collectibility.

Key Facts You Should Know

- You must file Form 656‑L (Offer in Compromise – Doubt as to Liability). IRS

- No detailed financial disclosure (Forms 433‑A/B) is required for a DATL because it’s not about ability to pay — it’s about correctness of liability.

- Submitting a DATL does not automatically stop collection (levies or liens) unless the IRS accepts the offer or stops collection by other means.

- The IRS will closely evaluate the evidence, and may judge whether the “hazards of litigation” (i.e., whether the IRS could lose in court) justify acceptance. IRS+1

Final Thoughts

A DATL OIC is for when you dispute the tax liability itself — not just the ability to pay. If you have legitimate grounds to challenge the amount assessed but missed the chance through the usual audit/appeal route, this resolution path may be your best option.

It’s not a workaround — it’s a built‑in IRS process for fair resolution. And if the tax truly isn’t correct, a carefully prepared DATL could save you thousands.

Need help deciding if this fits your situation, or want help preparing the supporting documentation? I’ve got you covered.

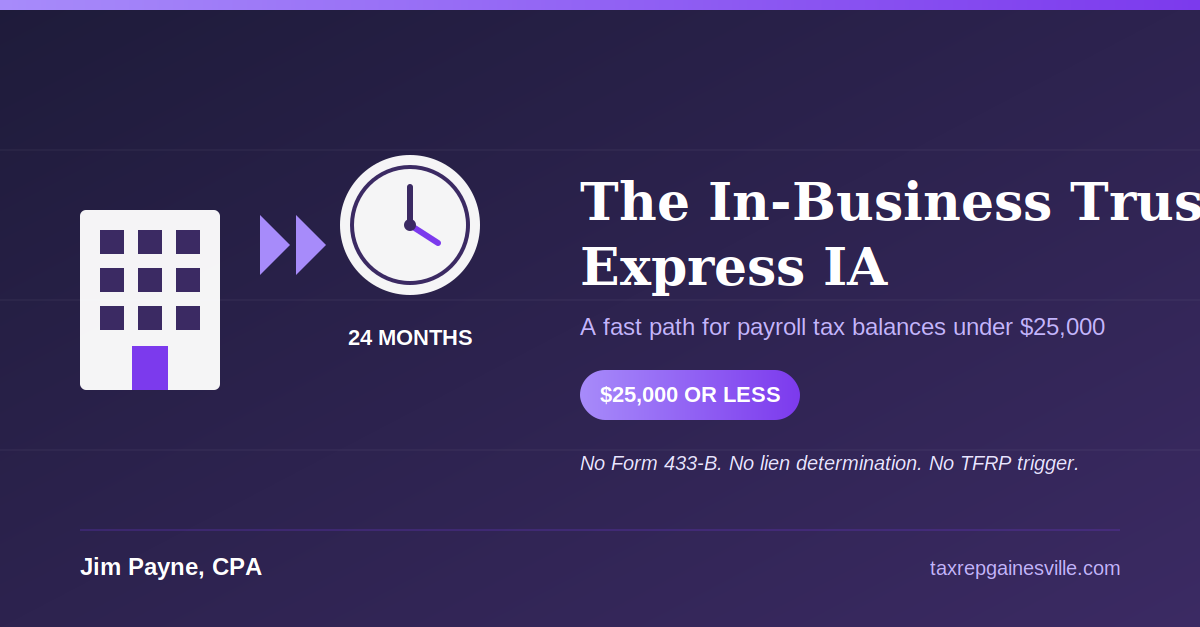

The In-Business Trust Fund Express Installment Agreement: A Fast Path for Small Payroll Tax Balances